TURKISH MINING INDUSTRY FACTS

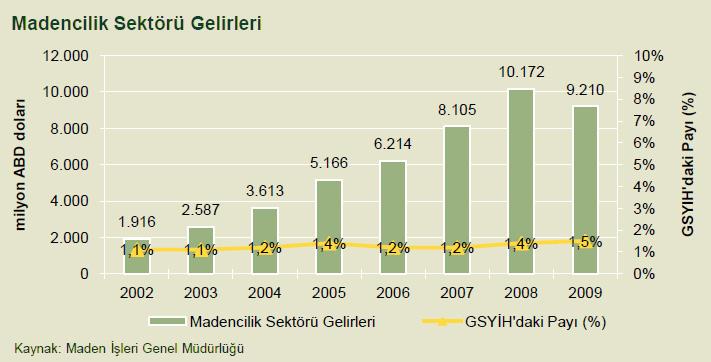

The Turkish mining sector achieved a remarkable CAGR of 32.1 percent between 2002 and 2008, with revenues that rose from USD 1.9 billion in 2002 to USD 10.2 billion in 2008. There was a modest decline to USD 9.2 billion in 2009. The sector's share in Turkey's GDP ranged between 1 and 1.5 percent, reaching a 4.2 - 4.9 percent1 share in the total industry during the past five years. These figures are low compared with the sector's importance; however, with the recovering economy and the increasing capacity of the manufacturing industry, together with the implementation of advanced mining technologies, the sector is likely to grow further.

Turkey is an important player in the international market due to its wealth of reserves, considerable production capacity and geographical advantages for transportation and shipping. Ranking 28th in global mining production, Turkey also ranks 10th by variety of mines and minerals.

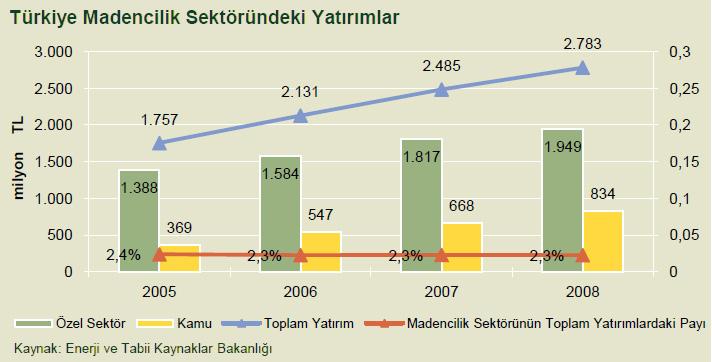

As part of the EU membership accession negotiations, the government started intense studies for liberalization and privatization in several industries, mining being one of the. With the regulatory changes, incentives offered, and reduced bureaucratic processes for obtaining mining licenses, both local and foreign investments have increased each passing year, reaching TRY 2. 78 billion in 2008, and are expected to continue growing in the coming years.

TURKISH MINING PRODUCTS

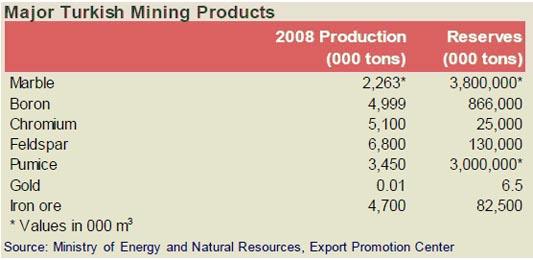

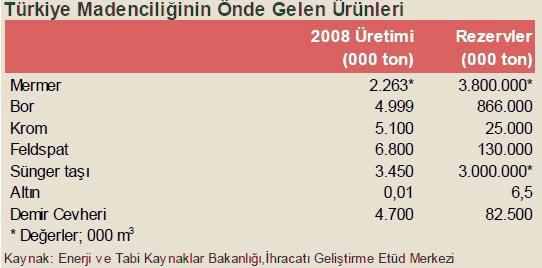

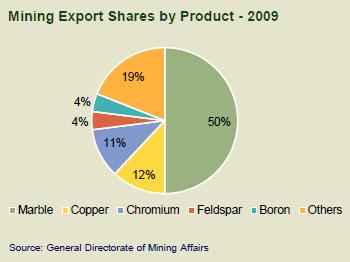

Turkey maintains a wide spectrum of mines and minerals and has considerable reserves. Marble and natural stones, boron minerals, chrome, feldspar, pumice, bentonite, pearlite, calcite and trona reserves are the most significant. Among these, Turkey's main exports are marble and natural stones, boron, chrome, feldspar and pumice.

In addition, there has been an important increase in the exploration and mining of metallic ores such as gold, silver, copper, chrome and manganese.

Turkey holdes 2.5 percent of the global industrial mineral reserves, 72 percent of global boron reserves, 33 percent of global marble reserves, 20 percent of global bentonite reserves and more than half of global pearlite reserves. 13 Turkey has 3,500 types of metallic and 2,000 types of mineral deposits. The minerals mined out of these deposits are used as raw materials in the manufacturing industry, while the surplus is exported.

TURKISH MINING INDUSTRY REVENUES

Mining industry revenues increased with a CAGR of 32. 1 percent between 2002 and 2008 and constituted approximately 1 - 1.5 percent of Turkey's GDP, reaching USD 10.2 billion in 2008, then falling slightly to USD 9.2 billion in 2009.

TURKEY'S EXPORTS IN MINING

With the liberalization and privatization of the industry and the incentives granted by the government in recent years, both local and foreign investments increased, which triggered an upward trend in production.

Besides the investments and changes in the economy, Turkey's geographical location allows the export of mining products at a relatively low cost.

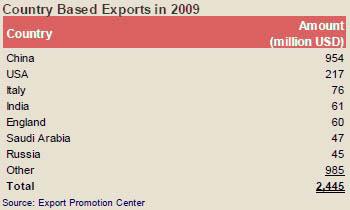

China, the USA, Italy, India, the UK, Saudi Arabia and Russia are the most important customers for Turkish mining products.

TURKISH MINING INDUSTRY OPPORTUNITIES

Liberalization and privatization of the mining industry and the incentives granted by the government will help the country develop a competitive and strong industry with major global players.

With the increasing FDI and entry of new foreign companies, the latest advanced mining technologies will be introduced and exploration investments will rise.

TURKISH MINING INDUSTRY INVESTMENT OPPORTUNITIES

In connection with the EU accession negotiations, the Turkish government speeded up liberalization and privatization in almost every industry, mining being one of them.

There are two types of licenses in the mining industry, both of them issued by the state. Due to the time-intensive procedure for getting a mining permission and license, as well as the high fees paid by the investors for these licenses, entries to the industry were limited. To overcome these obstacles, various departments involved in the licensing process were reorganized under the Mining Affairs General Directorate of the Ministry of Energy and Natural Resources and the fees were reduced.

Moreover, in March 2009, the government introduced new tax advantages. 37 As a result of these changes, investments in the mining sector increased with a CAGR of 16.6 percent between 2005 and 2008, constituting about 2.3 - 2.4 percent of all the investments.

TURKISH MINING INDUSTRY - FDI

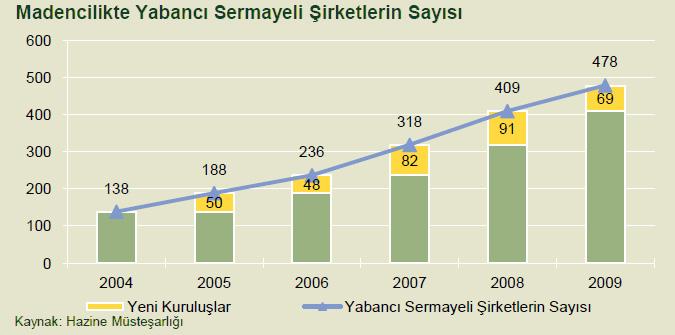

FDIs in the Turkish mining industry were around USD 193 million in 2009, equaling 3.3 percent of the total FDI. The number of companies with foreign capital in the mining industry increased every single year and reached 478 in 2009.

TURKISH MINING INDUSTRY FACTS - IRON ORE

Turkey carries an estimated 82.5 million tons of iron ore reserves most of which are found in the provinces of Balikesir, Sakarya, Kirsehir, Adana, Hatay, Kayseri, Sivas, Erzincan, Malatya and Bingol.

The production of iron ore in Turkey has not changed significantly throughout the years due to the insufficient level of reserves. Turkey produced 4.7 million tons of iron ore in 2008, while this figure was 4.6 million in 2005.

Due to the low iron ore production Turkey is dependent on iron ore imports. Since Turkey has a very substantial steel industry, the iron ore imports are considerable.

In 2012, Turkish iron ore imports rose by 18% and reached 7.8 million ton according to the Turkish Statistical Institute (TUIK). The value of iron ore imports was USD 1.15 billion.

In 2012, Brazil constituted 58% of Turkey’s total iron imports with 4.6 million mt. Sweden constituted 15% , Russia constituted 9.2% and Ukraine constituted 8,9% of Turkey’s iron ore imports. Canada, South Africa and other countries constituted remaining 8,4% of the imports.

KEY FACTS AND FIGURES

- 2nd largest producer of steel in Europe

- 10th most imortant steel-producing country globally

- 3rd fastest growing steel producer globally between 2001 and 2010

- World's leading exporter of reinforced bars

- The European Union is a major export market for Turkish steel

- 72% of Turkish crude steel production belong to scrap consuming EAF mills

- Largest scrap consumer in Europe (25.3 million tonnes) in 2010

- World's largest importer of scrap metal

- Net importer of iron ore

TURKISH MINING LINKS

- Ministry of Energy and Natural Resources (ETKB) http://www.enerji.gov.tr

- Mineral Research and Exploration General Directorate (MTA) http://www.mta.gov.tr

- General Directorate of Mining Affairs (MIGEM) http://www.migem.gov.tr

- Istanbul Minerals And Metals Exporters Associations (IMMIB) http://www.immib.org.tr

- Chamber of Mining Engineers Of Turkey (MADEN) http://www.maden.org.tr